Commercial Wisdom: The Myth I Watched From Outside the Room

The law makes the Committee of Creditors’ “commercial wisdom” supreme and almost beyond review. I sat in those meetings — and for half of them, I was sent out of the room.

There is one phrase that decides the fate of almost every company that enters insolvency in India: the “commercial wisdom” of the Committee of Creditors. The Supreme Court has held, again and again, that this wisdom is supreme — that the tribunals cannot second-guess it. I sat in those meetings. So let me tell you what that wisdom actually looked like, from the inside.

Half the time, I was asked to leave the room

I was the one person in that process who had built the company — who knew its products, its plants, its people, its customers. And for a good half of those meetings, I was asked to step outside, because the committee had things to discuss that they did not want me to hear or to present on.

Think about that. The body deciding the future of the company sends out the only person who actually understands it. Whatever “wisdom” was being exercised, it was being exercised with the door closed on the one source of real knowledge in the building.

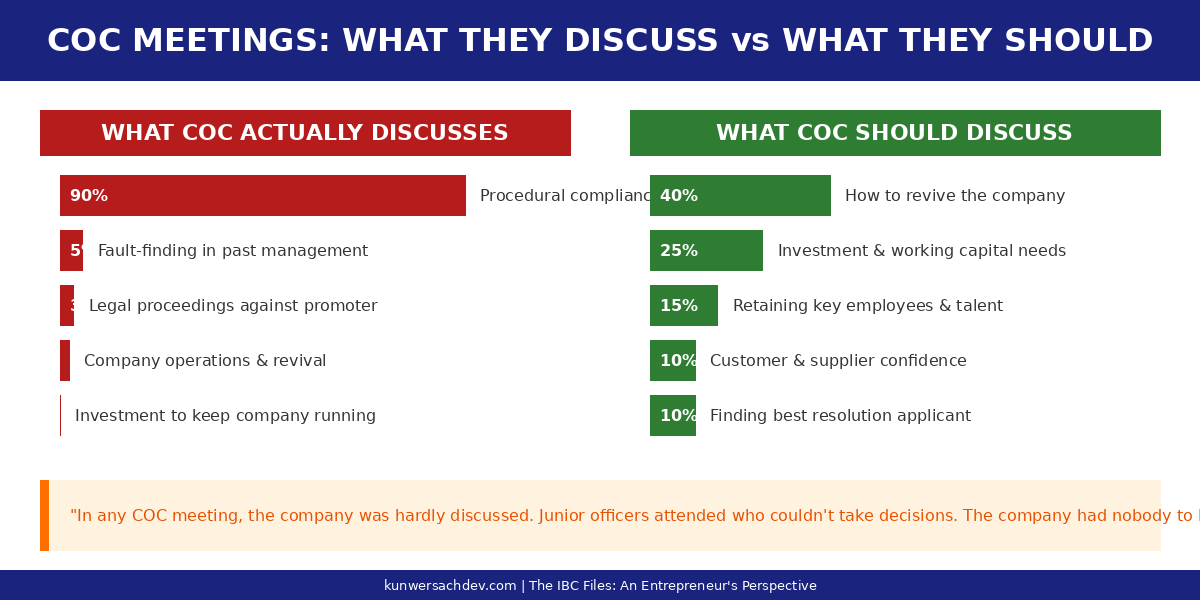

Not once did a banker ask about operations

In all those hours, across all those meetings, I never saw a single banker ask the questions that actually decide whether a company lives or dies. How are the plants running? What is happening to the order book? Which products are still selling? What does the team on the ground need to keep going? Not once. The conversation was about numbers on paper, votes, approvals, recoveries — never about the living, breathing business those numbers came from.

They watched their own guarantees burn

And then came the moment I will never forget. In front of me, bank guarantees for our projects were being revoked — and the bankers simply watched it happen. Nobody picked up the phone. Nobody went to the project site to see how those guarantees could be protected. These were their own guarantees, their own exposure, their own money walking out the door.

If they would not lift a finger to save their own bank guarantees, what chance did the day-to-day operations of the company ever have? That is when I understood: this was not a rescue. It was a process being administered by people with no stake in whether anything was actually saved.

They stopped my salary — and the company began to die

In one of those meetings, they stopped my salary. They did it, I believe, without even pausing to realise that the company was my only source of income — I had nothing else. From that day, I lost everything. And so, in a way, did the company.

Because it sent a message to every single person in that building: if they can do this to the founder, then tomorrow it can be any one of us. Within three months, almost everyone who could actually have saved the company had left to look for other jobs. The people you need most in a rescue are the first to read the writing on the wall — and they were right to read it.

The cruellest loss of all was the R&D team I had built and nurtured for more than twenty years. They were the engine of everything — the 77 patents, the firsts, the technology that defined Su-Kam. One by one they left, and many of them joined our competitors, carrying two decades of hard-won knowledge straight to the rivals. The innovation did not merely stop; it walked out of the gate and went to work for someone else.

Complete power, zero responsibility

This is the deepest flaw of all. The committee, and the process around it, holds complete power to do anything to anyone in the company — and no responsibility to actually perform. Look at what happened on their watch, with no one answerable for any of it:

- The company’s balance sheets were not filed with the Registrar of Companies for almost four years — because it was no one’s job.

- The patents — the very technology the company was built on — were allowed to lapse, including the 77 patents we had built over the years.

- Sales fell to a third of what they had been.

- Bank guarantees were forfeited.

- Service collapsed, and the brand we had spent decades building was tarnished.

- Suppliers went unpaid. Employees went unpaid.

And yet — the lawyers, the Resolution Professional and PwC were paid on time, every time. Under the IBC’s own waterfall, the costs of the process rank first. So the one group guaranteed to be paid were the people administering the decline; the people who had actually built the company — its workers, its suppliers — were left waiting. That is the equation at the heart of this system: total authority on one side, total absence of accountability on the other.

Who are these people, really?

I want to be fair to the bankers, because the problem is not the individuals. It is the design. People who work in banks have a very particular kind of knowledge. They are financially driven; their core job is giving loans and watching systems and processes. When a banker sanctions a loan, he is rarely looking physically at the business — it is paperwork, fed into a system. A real physical audit of a company is simply not possible at that scale. So a balance sheet and a few documents required for lending do not mean the banker understands the business. They were never trained to.

And even in the room, they cannot really decide. A bank officer on a Committee of Creditors needs approval from his Head Office for almost any fresh financial commitment. So he is careful, procedural, and above all anxious to keep his own position clean. The same officers, meanwhile, are sitting on the committees of many companies at once. No one is responsible for the operations of any single one of them. The Resolution Professional is not responsible for running the business either. And the promoter — the one person who is — is treated as the villain and pushed out, as I described from inside the CIRP.

So ask the simple question I kept asking: in that room, who is actually capable of running the company?

No training, no system, no contact with the team

It gets worse the closer you look. There is no training by which bankers are prepared to conduct these meetings — no standard method, no playbook for steering a living company through crisis. There is no system to collate the company’s operating data and make sure it is improving week on week. There is no interaction with the core team that actually runs the company day to day.

So I ask, honestly: where is the synergy for such a meeting to ever be fruitful? You remove the people who understand the business, bring in people who were never meant to run one, give them no training and no data and no contact with the operators — and then declare their judgment to be supreme wisdom.

And yet — it is untouchable

Here is the part that turns a flawed process into an injustice. The law has placed this committee’s judgment beyond review.

In K. Sashidhar v. Indian Overseas Bank (2019), the Supreme Court held that the commercial wisdom of the CoC is non-justiciable — the tribunals cannot sit in appeal over it. In the Essar Steel judgment later that year, the Court again affirmed that the CoC’s commercial wisdom is paramount, and that the NCLT and NCLAT have only a narrow window to interfere. Questions of viability, valuation and how much creditors will write off are treated as purely commercial — and so the courts step back.

In principle, that restraint makes sense: judges should not run businesses. But look at what it means in practice. We have taken a body that, as I have described, often has no operational knowledge, no accountability for the company, no training and no real authority of its own — and made its decisions almost impossible to challenge. Supreme power, handed to a committee with no responsibility for the outcome.

I took it to court — and the High Court agreed

I did not just carry this grievance in private. I took it to the Delhi High Court.

In Kunwer Sachdev v. IDBI Bank & Ors., the Court looked at exactly what I had lived through and found something remarkable: that there existed no code of conduct, no guidelines at all for how the Committee of Creditors was supposed to function. In February 2024 it directed the IBBI to frame one within three months.

Sit with that for a moment. The body whose “wisdom” is treated as supreme and beyond challenge had been operating, for years, with no rulebook whatsoever. A High Court had to step in and order one to be written.

And what came of it? The IBBI duly issued its “Guidelines for Committee of Creditors” in August 2024. I will be honest about what I think of them: to my eyes they were so thin and toothless that reading them is almost comic — a box-ticking answer to a structural problem, drafted to satisfy the court rather than to fix anything. By then I had no money left to keep fighting, and I wanted my life to be peaceful. So I stopped. But anyone who reads what was actually submitted will struggle to keep a straight face.

So who runs the company there — do the bankers?

No. And that is the whole point. In neither the United States nor the United Kingdom do the lending bankers run the company. In the US it is run by the company’s own management; in the UK, by a trained, licensed professional. The lenders have a powerful say — but they are not handed the wheel.

The contrast with the systems we copy our laws from could not be sharper. In the United States, under Chapter 11, the people who actually run the business — the existing management — usually stay in control as the “debtor in possession,” and the court tests any plan for feasibility and fairness before confirming it. The operators stay at the wheel, and a judge checks the work.

In the United Kingdom, the company is handed to a licensed, regulated, trained insolvency practitioner whose entire profession is rescuing or winding down businesses — not to a rotating cast of loan officers.

Only in India do we take operational control away from the people who understand the business, hand it to bankers who were never trained for it, and then place their “wisdom” above the reach of the courts.

“You remove the people who understand the business, bring in people who were never meant to run one — and then call their judgment supreme wisdom.”

Make the wisdom real

I am not arguing that creditors should have no say — of course they must. I am arguing that if we are going to call it wisdom and make it supreme, then we have to make it real:

What would make the committee actually work

- Put operational expertise inside the committee — people who have actually run companies, a turnaround cell whose job is the business, not just the recovery.

- Keep the management and promoter at the table, not outside the door — under scrutiny, but in the room — so the people who know the company can inform the decisions about it.

- Build a real data system: the operating numbers collated and reviewed every week, with a duty to show whether they are improving.

- Train the bankers and give them a standard process for steering a company in distress, instead of leaving each officer to protect his file.

- Add a thin layer of accountability — a narrow review not of pure commercial judgment, but of whether the committee even applied its mind to the operations and the value it was meant to protect.

What I learned from outside that door

“Commercial wisdom” is the most quoted phrase in Indian insolvency. It is invoked to end arguments, to shut down appeals, to justify whatever the committee decides.

From the other side of that closed door — sent out of my own company’s meeting, watching guarantees revoked while no one moved — I learned that the phrase can be the emptiest in the entire Code. There was a great deal that was commercial in those rooms. I am still looking for the wisdom.